Related insights

The DXY Index depreciated by 0.8% to 107, testing the upper boundary of its previous two-year range. The greenback’s pullback from its mid-January peak has been attributed to US President Donald Trump’s slow rollout of tariffs and the subsequent decline in the US Treasury 10Y yield down towards 4%. Additionally, Trump’s unexpected move to engage his Russian counterpart in efforts to end the war in Ukraine added further pressure on the USD. Barring further surprises, there are reasons for the DXY to consolidate around present levels.

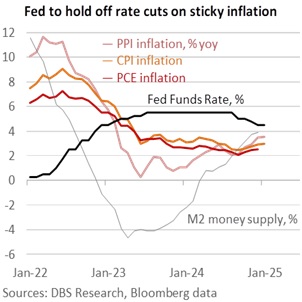

First, the US Treasury 10Y bond yield is approaching 4.50% or the ceiling of the Fed Funds Rate range(4.25-4.50%). Fed Chair Jerome Powell will be looking for PCE inflation on February 28 to mirror the upside surprises in PPI and CPI inflation. Yesterday, PPI inflation was faster than expected at 0.4% in January vs. the 0.3% consensus. December was also revised to 0.5% from 0.2% previously. During his semi-annual congressional testimonies this week, Powell also told US lawmakers that a sharp increase in M2 money supply might result in some inflation.

Second, Trump’s tariffs are still coming. The 10% tariff on Chinese imports proceeded as scheduled on February 4. Canada and Mexico are still at risk of 25% tariffs on their exports to the US after the one-month reprieve granted on February 3 expires. Given the need for additional revenue to fund the extension of tax cuts expiring this year, Trump will require more than tougher border measures to curb drug trafficking and illegal immigration to rescind the tariff threat. On Monday, Trump announced a 25% tariff on steel and aluminium imports, effective March 12. Yesterday, Trump directed the Trade Representative and Commerce Secretary to propose reciprocal tariffs on each of America’s trading partners to rebalance bilateral trade deficits, which Commerce Secretary nominee Howard Lutnick said should be ready by April 1. In signing this directive, Trump also made good on his strong intent to impose tariffs on the EU.

Third, reality will likely set in regarding the Trump administration’s recent initiative to end the war in Ukraine. His unexpected move to directly engage Russian Vladimir Putin has elicited strong reactions and raised significant concerns. Ukraine and European allies fear their exclusion from the negotiations could result in possible concessions favouring Russia and weakening NATO’s collective security framework. Trump’s suggestion for Russia to be readmitted into the G7 is unlikely to be well received by them either.

Quote of the Day

“If I had a flower for every time I thought of you, I could walk through my garden forever.”

Alfred Lord Tennyson

February 14 in history

The Australian dollar was decimalized in 1966, replacing the Australian pound.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

Related insights

- Member of Central Deposit Insurance Corporation (CDIC)